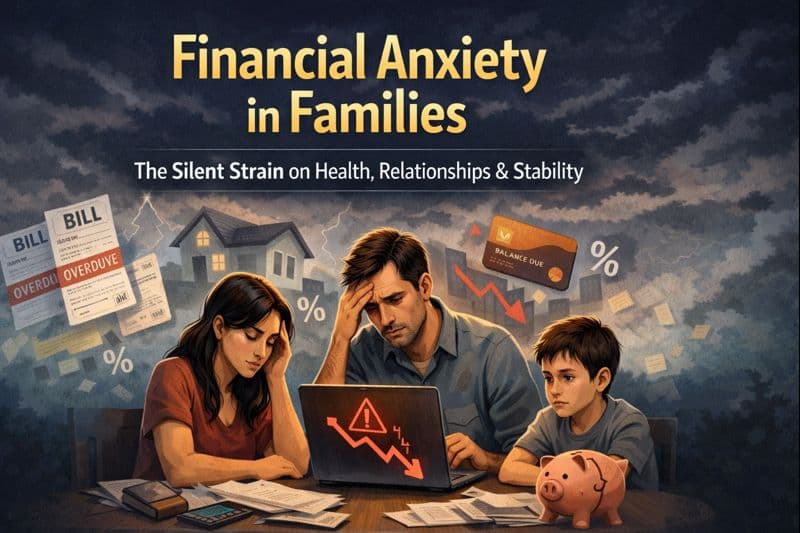

The Hidden Cost of Financial Anxiety in Families

Why money stress quietly drains health, relationships, and long-term stability

Search for a command to run...

Why money stress quietly drains health, relationships, and long-term stability

No comments yet. Be the first to comment.

A funny, Loki-inspired guide for middle-class families, expats, NRIs, and small business owners who want their income, expenses, assets, liabilities, and goals to finally converge.

A reflective personal finance journey about budgeting, debt, wealth building, financial discipline, and how middle-class families can achieve peace through smarter money management with deterministic AI tools like Amifi.

A practical guide to managing money, avoiding financial drift, and building long-term stability

In today’s world, financial advice is everywhere. Social media, YouTube, WhatsApp forwards, even AI tools. But here’s a simple truth most people miss: 👉 Not every confident voice is a reliable guide.

What Middle-Class Must Negotiate vs Protect - In a world negotiating oil, you must negotiate your money

Most families think financial stress is about not having enough money.

In reality, it is about not feeling in control of money.

Two households with the same income, same expenses, and same assets can experience wildly different levels of anxiety. One feels stable. The other feels constantly on edge. The difference is not income. It is visibility, predictability, and confidence.

Financial anxiety is rarely dramatic. It is quiet, persistent, and deeply expensive.

Money stress does not switch off when the banking app closes.

It shows up at dinner tables, in late-night conversations, and in the background of every major family decision. Parents carry it into work. Children absorb it without understanding it. Couples feel it long before they talk about it.

The real cost is not just emotional. It compounds over time.

When families live with ongoing financial anxiety, they tend to:

Avoid looking at finances to reduce stress

Delay important decisions like insurance, education planning, or investing

Overreact to short-term expenses

Undersave because planning feels overwhelming

Argue more often about money even when numbers are manageable

Anxiety changes behavior before it changes balances.

Many families start their financial journey with expense tracking. It feels logical. Measure first, fix later.

But expense tracking alone often increases anxiety instead of reducing it.

Most apps show spending in isolation. Charts go red. Budgets show overspending. Notifications highlight what went wrong, not what is stable.

Apps like Mint or YNAB work well for individuals who already enjoy managing money. For families with multiple incomes, shared responsibilities, loans, assets, and long-term goals, constant expense focus creates pressure without context.

Knowing you spent more this month does not help if you do not know:

Whether your overall cash flow is healthy

How assets and liabilities balance out

If long-term goals are still on track

Whether this month is an exception or a pattern

Without context, tracking feels like surveillance. Anxiety grows.

Most finance tools focus on one pillar at a time.

Some apps track expenses well. Others track investments beautifully. Loan apps focus only on EMIs. Bank apps show balances but no direction.

Very few systems help families see everything together.

When assets, income, expenses, liabilities, and goals live in separate apps, the brain fills gaps with worry. Families start guessing instead of knowing.

Common silent questions appear:

Are we actually doing okay?

Can we afford this decision?

What happens if one income pauses?

Are we saving enough or just hoping?

Unanswered questions create anxiety even when numbers are fine.

Money stress spreads.

One anxious partner often becomes the default financial decision maker. The other disengages. Children sense tension but lack explanation. Over time, money becomes a taboo topic instead of a shared system.

This is how financial anxiety creates long-term damage:

Children grow up associating money with fear or conflict

Couples avoid financial conversations until crisis points

Short-term comfort purchases replace long-term planning

Families delay wealth-building because clarity never arrives

None of this is caused by lack of intelligence. It is caused by lack of calm systems.

Modern finance apps love dashboards.

But more charts do not equal more clarity.

Families do not need more data. They need fewer decisions, better framing, and clearer signals.

Investment-only platforms like Zerodha Coin or Groww show portfolio performance well, but they do not explain how investments relate to household cash flow, EMIs, or upcoming obligations.

Expense-only apps show where money went, but not where the family is going.

Anxiety reduces when families can answer one simple question confidently:

“Are we financially okay right now, and are we moving in the right direction?”

Financial calm does not come from perfect discipline.

It comes from:

Knowing where money stands today

Understanding how today affects tomorrow

Seeing progress even when life is messy

Trusting the system even during irregular months

Families with financial calm do not obsess over every transaction. They make better decisions because anxiety is not driving them.

This is the difference between managing money and being managed by money.

Families need systems that reduce cognitive load, not increase it.

That means:

Seeing income, expenses, assets, liabilities, and goals together

Fewer alerts, more insight

Context before judgment

Trends over time, not daily noise

Support for shared family realities, not solo optimization

Financial anxiety is not solved by discipline alone. It is solved by design.

Unchecked financial anxiety quietly steals:

Mental energy

Relationship quality

Long-term wealth

Confidence in decision-making

Peace of mind

And none of it shows up in monthly summaries.

Building a calm financial system is not about becoming perfect with money. It is about making money stop feeling like a constant threat.

This is the gap most finance apps still fail to address. And this is the problem Amifi is being built to solve.