₹13 Lakh Crore Gone in a Day: What Most Investors Still Don’t Understand About Market Crashes

Valuation Shock, Derivatives Risk, and Why Panic Selling Destroys Middle-Class Wealth

The headlines are dramatic:

₹13 lakh crore wiped out

Sensex down ~1900 points

Nifty slipping below 22,500

But if you look deeper, today wasn’t just a market fall.

It was a valuation reset.

And this is where most middle-income investors get caught off guard.

What Really Happened Today: It’s Not Just Fear — It’s Repricing

Markets don’t fall randomly.

They fall when assumptions break.

Today, multiple assumptions got questioned at once:

Growth expectations (due to war, oil shock)

Liquidity expectations (US policy uncertainty)

Cost structures (inflation risk)

And when that happens:

Valuations adjust instantly — even if the business hasn’t changed yet.

The Hidden Trigger: Valuation Compression (PE & PEG)

Let’s simplify what most people ignore.

1. Price-to-Earnings (PE) Ratio

High PE = market expects strong future growth

Low PE = stable or slow growth expectations

Example:

Stock trading at PE 40 → market assumes strong growth

If growth outlook weakens → PE falls to 25

Even if earnings stay same:

Stock price can drop 30–40% just from valuation correction

2. PEG Ratio (Growth Adjusted Valuation)

PEG = PE ÷ Growth rate

PEG ~1 → fairly valued

PEG >1.5 → expensive (growth expectations high)

Now think about today:

War → growth uncertainty

Oil → cost pressures

US tightening → slower global demand

So growth estimate drops.

Which means:

PEG shoots up → stock suddenly looks expensive → selling begins

Real Example (What Just Happened)

A stock at PE 50 with expected growth 25% → PEG = 2

Growth revised to 15% → PEG = 3.3

Now market reacts:

Either growth must improve

Or price must fall

Markets choose the second → price crashes

Why This Hits Middle-Class Investors the Hardest

Because most portfolios are:

Built during bull markets

Bought at high valuations

Concentrated in “popular” sectors

So when valuation resets:

Losses feel sudden

Confidence collapses

Panic selling begins

The Dangerous Layer: Derivatives (F&O) Amplify the Damage

Futures & Options Are Not Investing — They Are Leverage

Let’s be very clear:

F&O is a trading instrument, not a wealth-building tool for most people

Why F&O Is Risky for Middle-Income Families

Leverage Multiplies Losses

₹1 lakh capital → exposure of ₹5–10 lakh Small market move → large capital wipeout

Time Decay Works Against You

Options lose value even if market doesn’t move

So you need:

Direction right Timing right Volatility right

All three together = extremely difficult

Emotional Pressure

Intraday swings Margin calls Overnight risk

This leads to:

Forced decisions, not rational decisions

Reality Check

Most retail F&O traders:

Lose money consistently Exit after capital erosion Re-enter during next bull phase

Cycle repeats.

Compare That With:

Fundamental Investing / Mutual Funds

1. No leverage

2. Time works in your favor

3. Compounding happens

4. Lower emotional pressure

Why Even “Safe Assets” Fall During Crises

Many people expect:

Gold ↑

Crypto ↑

Stocks ↓

But reality is more complex.

What Happens During Panic Phases?

1. Liquidity Crunch

Investors sell everything to raise cash:

Stocks

Gold

Crypto

This causes:

All assets falling together temporarily

2. Flight to Safety

Eventually money moves to:

Cash / bank deposits

Government bonds

Dollar assets

3. Gold vs Crypto Behavior

Gold: stabilizes after initial fall, acts as hedge

Crypto: behaves like high-risk asset → falls with equities

Key Insight

In early panic → correlation = 1 (everything falls)

In recovery → differentiation begins

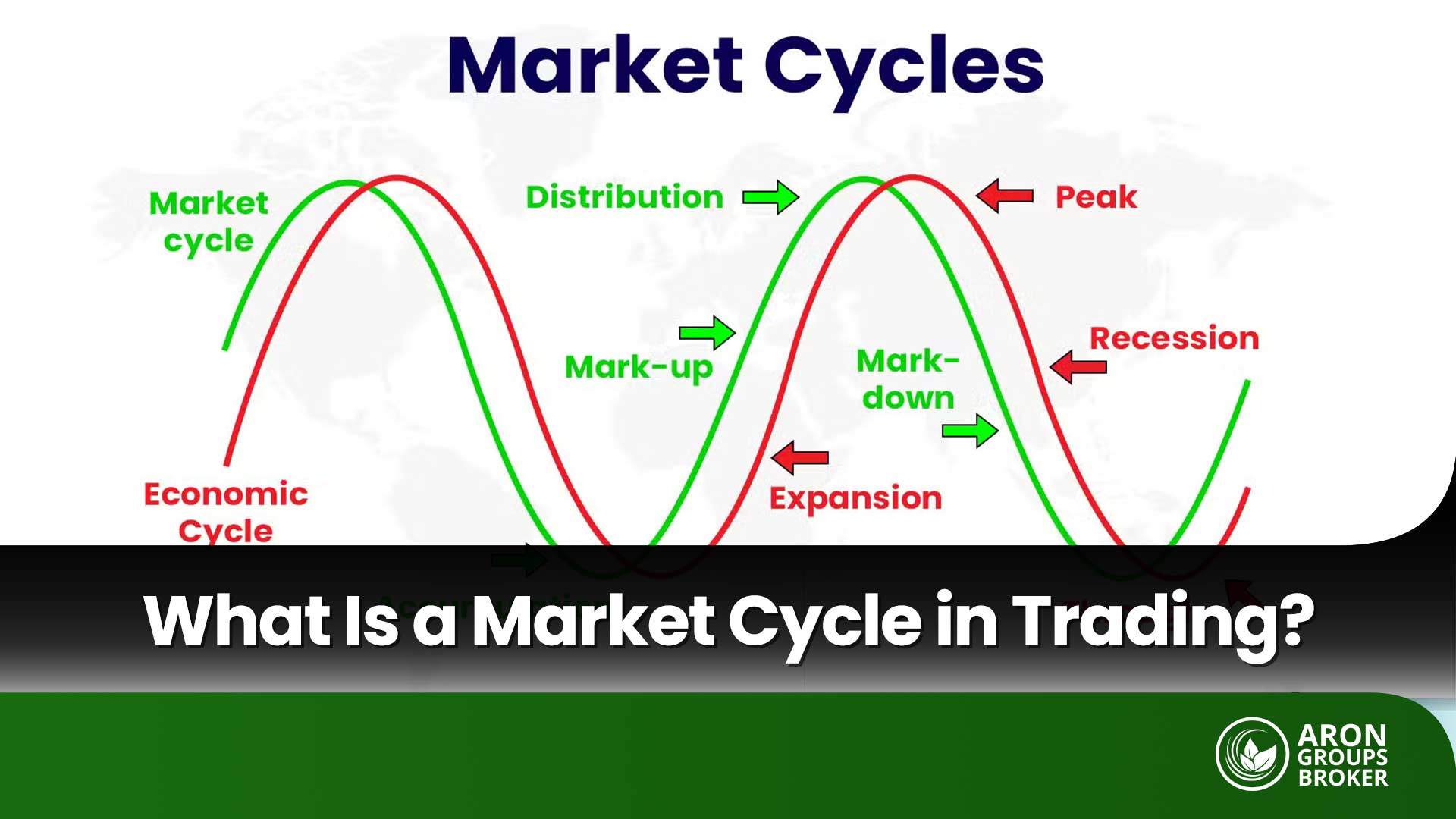

How This Will Likely Play Out (Scenario View)

Next 48 Hours (High Uncertainty)

US decision → volatility spike

Oil movement → sector-specific shocks

Markets remain unstable

Next 2–4 Weeks (Price Discovery Phase)

Earnings expectations revised

Valuations reset

Weak hands exit

Next 3–12 Months (Recovery Phase)

Stability signals emerge

Capital flows return

Strong businesses recover first

Historical Pattern

Every major fall follows:

Panic

Capitulation

Stabilization

Recovery

The Core Mistake: Mixing Strategy with Emotion

Most investors:

Buy based on growth stories

Sell based on fear

Instead of:

Buying based on valuation

Holding based on structure

What You Should Do Instead

1. Re-evaluate Entry Points (Not Just Prices)

Ask:

At current price, what is the PE?

What growth is realistically achievable now?

Is PEG still justified?

2. Avoid Leveraged Exposure

If you’re in F&O:

Reduce immediately

Treat it as speculative capital only

3. Strengthen Your Base

Emergency buffer

Diversified allocation

Liquidity planning

4. Accept This Truth

Good investments bought at wrong valuations still lose money

Why This Is Hard to Manage Manually

To make correct decisions today, you need:

Portfolio valuation tracking

Growth expectation understanding

Asset allocation visibility

Liability awareness

Cash flow clarity

Across multiple apps, accounts, and markets.

Most people:

Guess

React

Overcorrect

Why Amifi Becomes Critical in Such Times

This is exactly where clarity matters.

Amifi helps you:

Track true net worth (not just portfolio)

Understand valuation exposure across assets

Maintain safety buffer beyond generic emergency funds

Avoid impulsive decisions

Because:

When you see the full picture, you don’t react to one red screen

Final Thought: Markets Correct Valuations. Investors Destroy Wealth.

Markets falling is normal.

But:

Overpaying in bull markets

Leveraging through F&O

Panic selling in crashes

That’s what destroys wealth.

If You Do One Thing Today

Don’t ask:

“Should I sell?”

Ask:

“Was my entry justified in the first place?”

Join the Debate

We’re discussing this live:

👉 r/EverydayWealth

Did you buy at high PE/PEG?

Are you exposed to F&O?

How are you handling this correction?